The rate didn't move at the June 17 FOMC, but the message did. New Fed chair Kevin Warsh ran his first meeting and raised the bar: the goal is no longer for inflation to "stabilize" — it's for it to fall. Inflation at a three-year high, a hawkish first signature, and the July prints that decide everything — all along a single line of tension.

Warsh's first meeting was more than a handover. The Fed held the target range at 3.50–3.75% for the fourth meeting running, but the real news was everything around the rate: the statement came back shorter, the forward-guidance language was gone, and the median dot plot now points to a hike in 2026 rather than a cut.

- Rate held — fourth consecutive hold in the 3.50–3.75% range

- Forward guidance removed — Warsh gave no projection of his own; the road map was deliberately blurred

- Dot plot shifted up — the median path now implies a hike in 2026, not a cut

Markets read it cleanly: the 2-year yield rose 14.4 basis points, equities fell, the meeting was priced hawkish. When Warsh said "fall," what he meant was how far the inflation numbers still sit from target.

Peak, or just a pause?

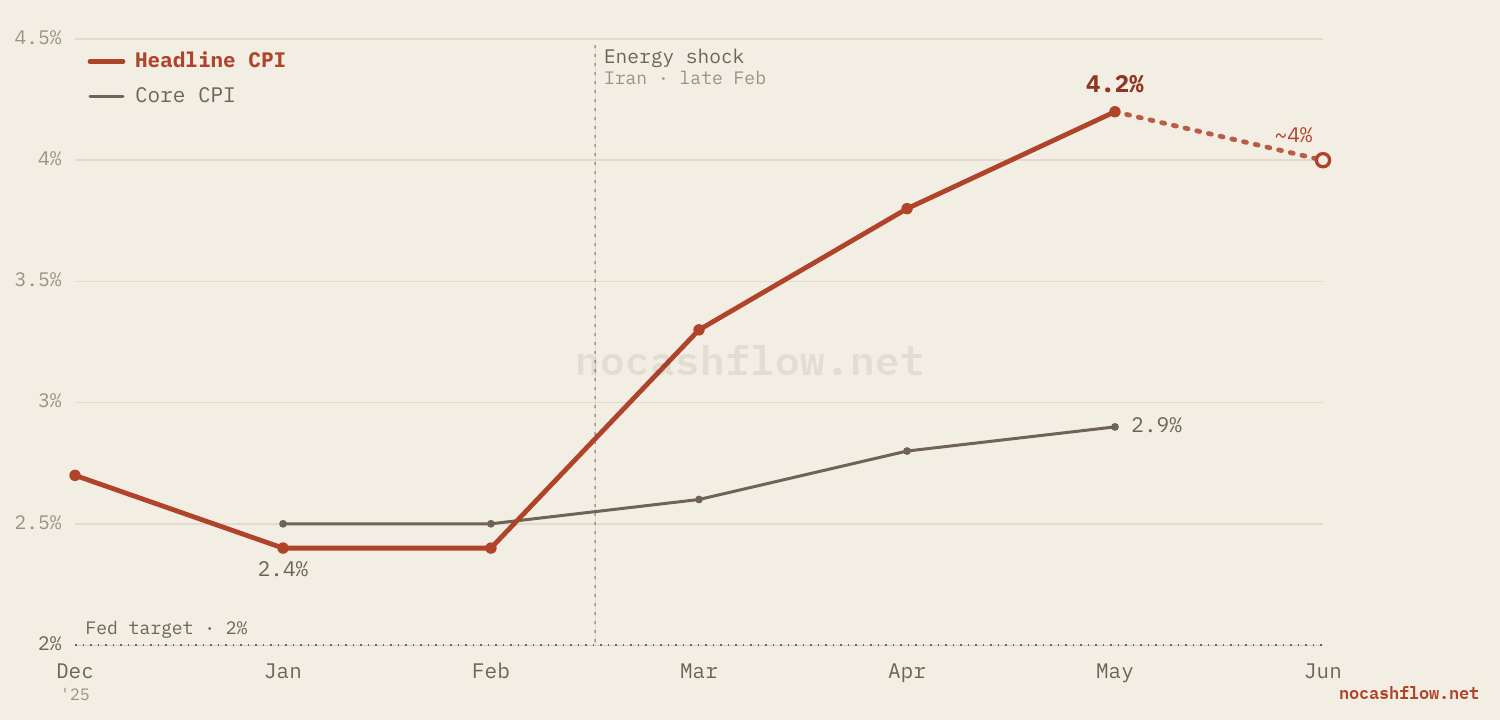

Headline CPI jumped from 2.4% in January to 4.2% in May — and the driver is almost entirely energy. An Iran-driven supply shock pushed energy prices higher from late February; gasoline ran above 40% year-over-year. Core CPI stayed far calmer over the same stretch: from 2.5% to just 2.9%. The gap between the two is the whole question — how much of this inflation is a passing shock, and how much is persistent pressure.

The latest snapshot confirms it. In May, headline PCE was 4.1% and core PCE 3.4% — even the Fed's preferred gauge sits well above target. Core came in line with expectations; headline ran a touch cooler month-over-month, but the level is still a three-year high. And demand is firm: income and spending both came in above forecast at 0.7%. You don't cut into that picture — and Warsh's statement says exactly that.

A Fed that won't tell you where it's going is usually a Fed looking for the answer in the data.

The data that matters next

The forward-guidance era ended quietly on June 17. From here we read the data, not the dots — and the July calendar is dense:

- ~Jul 2–3 · June payrolls (NFP): can the labor market carry a hawkish hike?

- Jul 14 · June CPI: consensus ~4.0% (Cleveland Fed). Below May would be the first cooling signal.

- ~Jul 28–29 · July FOMC: the market prices the first hike not in July, but in September.

- Jul 30 · June PCE + Q2 GDP: the Fed's preferred gauge and the first read on growth.

So what should you expect?

Rather than manufacture scenarios, it's more honest to ask the right questions. Three stand out: if June CPI comes in below 4%, does the "peak is in, the Fed waits" case strengthen? If inflation eases but employment weakens, does the Fed's job get harder rather than easier? And if the data sticks at 4%, does Warsh's "make it fall" bar put a September hike on the table? The answer starts arriving on July 14.